Risk in financial institutions no longer moves at the pace of a quarterly review cycle. Transaction volumes surge in milliseconds, third-party integrations multiply attack surfaces overnight, and regulators issue updated guidance with a frequency that strains even the most disciplined compliance teams. Manual processes cannot keep pace with high-frequency markets, evolving regulations, and massive data volumes, making automated risk management not a competitive advantage but a baseline operational necessity. This article examines the specific pressures driving that reality, the regulatory framework you need to navigate, and the concrete steps your institution can take to move forward with confidence.

Table of Contents

- The shifting risk landscape for financial institutions

- Why manual risk management falls short

- How automation and AI transform risk management

- Regulatory drivers: What compliance officers need to know

- Making the transition: Best practices for adopting automation

- The uncomfortable truth: Why partial automation isn't enough

- Accelerate your risk transformation with AI-powered solutions

- Frequently asked questions

Automate Regulatory Model Risk Governance

Examine models against 32 qualitative criteria and resolve risk Tiers with pre-deployment checklists per OCC 2011-12 guidelines.

Key Takeaways

| Point | Details |

|---|---|

| Manual processes can't keep up | Traditional risk management is too slow for today's fast-changing financial threats. |

| Automation delivers real-time insights | AI-driven tools detect and respond to risks immediately, minimizing losses and compliance breaches. |

| Regulations demand ongoing monitoring | SR 11-7 and GAO guidance require financial institutions to implement continuous, automated oversight of AI models. |

| Hybrid approaches optimize oversight | Combining automation with human judgment helps mitigate AI risks and ensures accountability in risk decisions. |

| Best practices ease adoption | Start with high-risk processes, leverage proven frameworks, and ensure board engagement for successful automation. |

The shifting risk landscape for financial institutions

After recognizing the need for automation, it's crucial to understand the specific risk challenges that drive this transformation. The risk environment confronting community banks and credit unions today is categorically different from what it was a decade ago. Digital transaction volumes have grown exponentially, real-time payment rails have compressed settlement windows to seconds, and the number of third-party vendors touching core banking data has multiplied with each new fintech partnership. Each of these developments introduces a new category of exposure that legacy controls were simply not designed to address.

Consider the compounding effect: a single community bank might process tens of thousands of ACH transactions daily, maintain integrations with a cloud-hosted core processor, a digital lending platform, and a mobile banking provider, while simultaneously monitoring compliance with BSA/AML rules, HMDA reporting obligations, and interest rate risk guidelines. Manual controls in that environment are not merely slow. They are structurally incapable of providing real-time visibility across all those risk vectors simultaneously.

Risk assessment models and AI have matured to the point where institutions of any size can access these capabilities, yet many community lenders and credit unions still rely on spreadsheet-based tracking and periodic manual reviews. The result is a growing gap between the speed at which risks materialize and the speed at which they are detected and addressed.

The table below illustrates how the risk environment has shifted across key dimensions:

| Risk dimension | Legacy environment | Current environment |

|---|---|---|

| Transaction velocity | Daily batch processing | Real-time, continuous |

| Regulatory update frequency | Annual guidance cycles | Ongoing, multi-agency |

| Third-party integration count | Minimal (1-3 vendors) | Extensive (10+ vendors) |

| Data volume per institution | Manageable manually | Petabyte-scale |

| Fraud sophistication | Static pattern-based | AI-driven, adaptive |

Automation provides proactive, scalable risk management essential for resilience in volatile markets, and institutions that delay this transition are effectively accepting expanding blind spots in their risk posture. For smaller financial institutions in particular, the scalability argument is decisive: automation allows a lean risk team to monitor and respond to a vastly larger set of exposures than any manual workflow could accommodate.

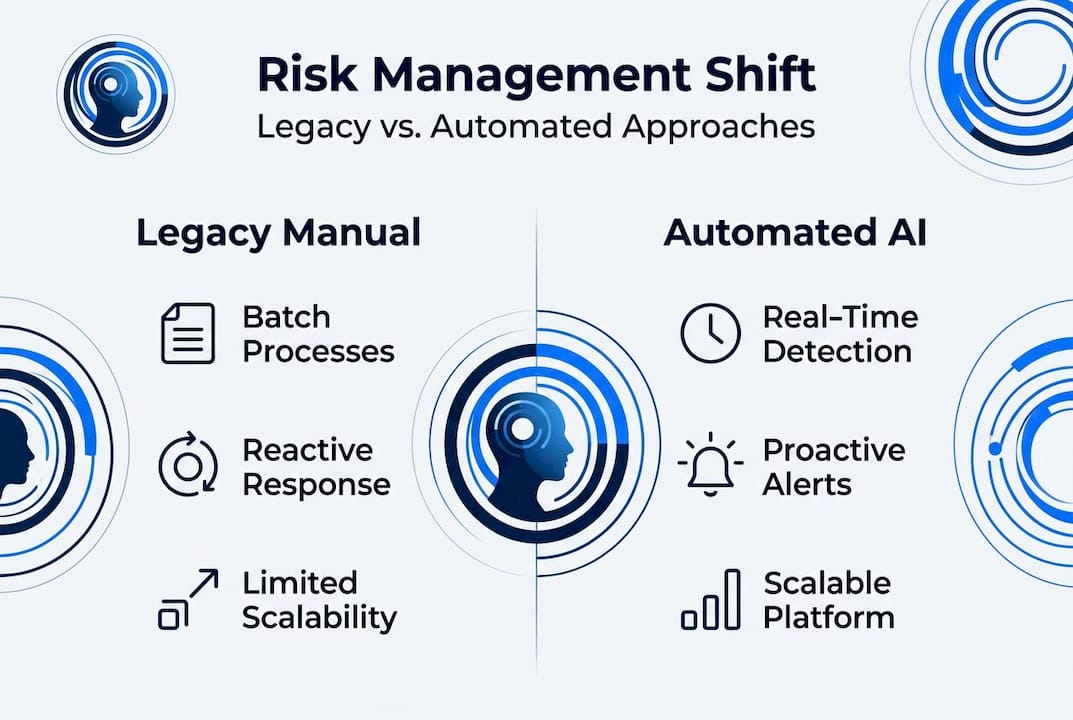

Why manual risk management falls short

With the landscape established, let's look at precisely why manual methods introduce unacceptable vulnerabilities and inefficiencies. The core problem is not that risk professionals lack skill or diligence. The problem is structural: manual processes are sequential, point-in-time, and capacity-constrained, while modern risk is concurrent, continuous, and volume-intensive.

A compliance officer running manual loan file reviews can reasonably process a limited number of files per day. At that throughput, a portfolio of several thousand loans cannot receive the regular scrutiny required to catch early warning indicators before they escalate into losses or examination findings. By the time a deteriorating credit is flagged, the institution may already be facing charge-off exposure or, worse, a regulatory finding tied to inadequate monitoring.

Manual processes lead to delays, errors, and non-compliance, and those delays carry measurable cost. Regulatory penalties tied to late or ineffective risk reporting have grown in both frequency and severity, with examiners at the NCUA and FDIC placing increasing emphasis on the timeliness and completeness of risk identification processes. An institution that cannot demonstrate real-time visibility into its risk position is, in regulators' eyes, an institution without adequate controls.

Consider the following failure modes common to manual risk workflows:

- Detection lag: Risk indicators identified in monthly reviews may reflect conditions that existed weeks earlier, well after mitigation windows have closed.

- Data aggregation errors: Manually consolidating data from multiple systems introduces transcription errors that distort the risk picture presented to management and the board.

- Capacity bottlenecks: Staff bandwidth limits how many counterparties, loans, or transactions can be reviewed in any given period, creating inherent coverage gaps.

- Audit trail gaps: Manual processes leave inconsistent documentation, complicating examiner review and making it difficult to demonstrate regulatory compliance.

- Reactive rather than predictive posture: Without algorithmic pattern recognition, manual teams can only respond to risks that have already become visible, missing leading indicators that predictive models would surface early.

Pro Tip: If your institution is still using spreadsheets as its primary risk tracking tool, start benchmarking your detection-to-response cycle time against peer institutions. That single metric will clarify the urgency of automation better than any theoretical argument.

AI-driven risk management addresses each of these failure modes with purpose-built capabilities, and understanding the mechanics of that improvement is what should drive your technology evaluation process.

How automation and AI transform risk management

After examining the failure points of manual systems, it's essential to clarify how automation and AI close those gaps and introduce new strengths that traditional frameworks simply cannot replicate. The performance differential is not marginal. It is categorical.

Automated risk platforms continuously ingest data from transaction systems, market feeds, regulatory databases, and third-party sources, running models against that data in real time and surfacing alerts before exposures escalate. Automation provides proactive, scalable risk management that responds to the actual cadence of modern financial risk, not the schedule of a human review cycle. The practical impact is measured in hours and dollars: faster detection means earlier intervention, and earlier intervention means lower loss severity.

AI specifically adds the capacity for adaptive learning. Where rule-based automation flags known patterns, machine learning models identify novel fraud vectors, emerging credit deterioration signals, and anomalous transaction clusters that no pre-programmed rule would catch. Some frameworks achieve 94.7% fraud detection accuracy, and regulators have noted that while these gains are significant, governance structures must accompany them to mitigate risks like model bias and cybersecurity exposure. This is precisely why hybrid human-AI models are considered optimal across both practitioner guidance and regulatory expectations.

The comparison below captures the operational difference at a practical level:

| Capability | Manual process | Automated and AI-enabled |

|---|---|---|

| Detection speed | Hours to days | Sub-second to minutes |

| Data coverage | Sample-based | 100% of transactions |

| Accuracy | Variable, human-dependent | Consistent, model-validated |

| Scalability | Constrained by headcount | Scales with data volume |

| Regulatory reporting | Manual compilation | Automated generation |

| Adaptive learning | Limited | Continuous model updating |

Key advantages AI-driven systems deliver for credit unions and community banks include:

- Real-time portfolio monitoring with automated exception flagging

- Consistent application of credit risk criteria across all loans, eliminating reviewer-to-reviewer variability

- Automated regulatory report generation that reduces manual compilation burden and associated errors

- Scenario modeling capabilities that allow risk teams to stress-test portfolios against adverse economic conditions

AI risk management best practices recommend coupling these technical capabilities with robust model governance from day one, not as an afterthought. Institutions that adopt automation without governance frameworks invite a different category of risk: model risk. Knowing this upfront allows you to build the right oversight structures before deployment rather than scrambling to retrofit them after an examiner raises concerns.

Pro Tip: When evaluating AI risk platforms, ask vendors specifically about their model validation processes, drift detection capabilities, and audit trail documentation. These are exactly the questions your examiners will ask, and your vendor's answers should align with advanced AI strategies that regulators view favorably.

Regulatory drivers: What compliance officers need to know

Even with the advantages that automation delivers, financial institutions must center their adoption strategy on compliance requirements, since the regulatory environment governing AI and automated models has grown more demanding and more specific in recent years.

SR 11-7, the Federal Reserve's foundational guidance on model risk management, establishes expectations for model development, validation, and ongoing monitoring that apply directly to AI and machine learning models used in credit decisions, fraud detection, and capital planning. The guidance requires that models be subject to independent validation, that their performance be monitored on an ongoing basis, and that governance structures exist to ensure appropriate oversight by qualified personnel and the board. For credit unions specifically, the GAO has recommended NCUA update model risk guidance to explicitly address AI-specific risks including algorithmic bias, data quality vulnerabilities, and privacy considerations.

The compliance obligations this creates are concrete and actionable:

- Model inventory maintenance: Every AI or automated model used in a risk decision must be cataloged, with documentation of its purpose, methodology, and validation status.

- Ongoing performance monitoring: Models must be monitored against defined performance benchmarks, with frequency calibrated to the model's risk tier.

- Independent validation: Model validation must be performed by parties independent of model development, with findings reported to senior management.

- Bias and fairness testing: AI models used in credit decisions require explicit testing for disparate impact and algorithmic bias, with documentation of testing methodology and results.

- Board and senior management engagement: Governance frameworks must include board-level awareness of material model risks and the controls in place to manage them.

Risk-tiered monitoring represents the current best practice: high-risk AI models should be monitored daily or weekly, with automated drift detection using Population Stability Index (PSI) and Characteristic Stability Index (CSI) metrics, and all model environments should be reproducible to support examiner review. Board oversight is not optional under SR 11-7. It is a prerequisite for compliance.

For compliance officers at credit unions and community banks, AI risk tools for compliance that embed these governance requirements directly into the platform architecture are materially easier to sustain than manual governance frameworks bolted onto automation after the fact. The regulatory trajectory is clear: AI in credit assessment and other model-driven risk processes will face increasing regulatory scrutiny, and institutions that build governance infrastructure now will be better positioned for examination cycles in 2026 and beyond.

Making the transition: Best practices for adopting automation

Now that the regulatory context is clear, let's look at how to navigate automation adoption step by step, grounded in expert recommendations and operational reality. The single most common mistake institutions make is attempting to automate everything simultaneously. That approach overloads staff, overwhelms change management capacity, and increases the probability of governance gaps.

The more effective path is disciplined and sequenced:

- Assess current workflows in detail. Map every risk process from detection to reporting, identifying manual steps, data handoffs, and decision points. This inventory becomes the foundation for prioritization.

- Prioritize by risk impact and regulatory exposure. Target the processes where manual delays create the greatest regulatory or financial risk first. Credit monitoring, BSA/AML transaction surveillance, and regulatory reporting are typically high on this list.

- Pilot automation on a defined scope. Select one or two high-priority processes and deploy automation with clear performance benchmarks and governance structures in place from launch.

- Train staff on both the tools and the governance expectations. Automation shifts human roles from data processing toward oversight and exception management, and staff need to understand both the technology and their new responsibilities.

- Establish model monitoring protocols before go-live. Risk-tiered monitoring and automated drift detection should be configured as part of initial deployment, not added later.

- Scale based on demonstrated results. Use performance data from the pilot to build the business case for broader automation, incorporating lessons learned into subsequent rollouts.

Proven AI risk management strategies consistently reinforce the importance of board engagement throughout this process. Risk and compliance officers who keep leadership informed and involved from the start encounter fewer governance challenges and build more durable automation programs.

Institutions that treat automation adoption as an IT procurement exercise rather than an organizational transformation consistently underperform. The technology itself is increasingly commoditized. The differentiator is the quality of the governance, training, and process redesign that surrounds it.

The uncomfortable truth: Why partial automation isn't enough

While best-practice steps provide useful guidance, there is a deeper organizational challenge that deserves a direct and honest assessment: partial automation, when it is the end state rather than a stepping stone, frequently makes risk management worse rather than better.

Here is why. When an institution automates credit monitoring but leaves regulatory reporting manual, or deploys AI fraud detection without integrating it into the broader risk dashboard, the result is a fragmented risk picture. Risk officers are managing two parallel workflows, one automated and one manual, and the seams between them become the new blind spots. Legacy vulnerabilities are not eliminated. They are relocated to wherever the automation stops.

Transforming credit union risk management through AI-powered intelligence requires an organizational commitment that goes well beyond technology selection. It requires process redesign, staff role redefinition, governance framework construction, and cultural acceptance that risk management is now a continuous, data-driven function rather than a periodic manual exercise. Industry leaders who have made this transition fully, not partially, have realized the compounding benefits: lower loss rates, faster regulatory response, and more confident board reporting.

The institutions that are falling behind are not the ones that lack technology access. They are the ones that adopted narrow automation and declared the job done. Genuine resilience comes from end-to-end integration, where automated detection, analysis, escalation, and reporting operate as a coherent system rather than a collection of disconnected tools.

Accelerate your risk transformation with AI-powered solutions

For institutions ready to modernize risk management, connecting a strategic plan to the right technology platform is the critical final step. RiskInMind's platform was purpose-built for exactly this moment, delivering an integrated suite of AI agents that automate credit risk assessment, regulatory compliance monitoring, and portfolio surveillance in a SOC 2 certified, bank-grade secure environment with response times under half a second.

Whether your priority is strengthening loan portfolio oversight with the CRE loan risk predictor, ensuring continuous regulatory alignment with the AI regulatory risk agent, or building an enterprise-grade AI-powered risk management program from the ground up, RiskInMind provides the AI infrastructure, governance architecture, and real-time intelligence your institution needs. Our solutions are designed specifically for credit unions, community banks, and lenders, meaning the workflows, compliance frameworks, and reporting capabilities are calibrated to your regulatory environment, not adapted from enterprise banking tools built for much larger institutions.

Frequently asked questions

What are the key regulations requiring automated risk management?

SR 11-7 and updated NCUA/GAO guidance mandate ongoing AI model monitoring, independent validation, governance frameworks, and board oversight, with explicit attention to AI-specific risks including algorithmic bias, data quality, and privacy.

How do automated systems improve risk detection speed?

Automated systems process data in real time, flagging emerging risks in seconds rather than the hours or days required by manual review cycles, closing the window between risk occurrence and institutional response.

Is human oversight still needed if risk management is automated?

Yes. Hybrid human-AI approaches are considered optimal by regulators, who stress that governance structures and human judgment remain essential to mitigate AI risks like model bias, cybersecurity vulnerabilities, and decision opacity.

Can small credit unions benefit from automation?

Absolutely. Automation delivers scalable, consistent risk controls that are especially valuable for resource-constrained institutions where a small risk team must cover a large portfolio with limited manual capacity.