In the shifting landscape of consumer finance, subprime unsecured lending — mainly credit cards and personal loans — has grown rapidly. Credit unions, fintech companies, and banks have filled the void left by stricter traditional lending standards. While this expansion improves credit access, it also raises red flags.

December 2025 data from TransUnion and Equifax shows delinquencies stabilizing at still-elevated levels. At the same time, turbulence in private credit — most visibly Blue Owl Capital’s permanent redemption halt on its OBDC II fund in February 2026 — points to potential funding vulnerabilities downstream.

| Category | Severe Delinquency Rate (60+ DPD) | YoY Change | Notes / Source |

|---|---|---|---|

| Overall Consumer Debt | 1.61% | +3 bps | Stabilizing; Equifax Dec 2025 |

| Credit Cards | ~3.0–3.5% | Mixed | Some segments down YoY; Equifax / TransUnion |

| Auto Loans | 1.61% | +3 bps | At or above GFC peaks in places; Equifax/TransUnion |

| Personal Loans | ~3.75% (forecast) | Stable | YoY improvement; TransUnion forecast |

| Mortgages | 1.36% (Q3 baseline) | +12 bps | Late-stage delinquencies rising; TransUnion |

| Subprime Segment | 11.4% (Q3) | -50 bps | Improved performance in high-risk tiers |

Maintain 100% NCUA & OCC Audit Readiness

Monitor regulatory updates 24/7, check internal credit policies, and generate compliance trails with Erina (AI Regulatory Agent).

1. The 2025 Credit Picture: Solid Overall, but Cracks Are Showing

By late 2025, total U.S. consumer debt stood at roughly $18.1–18.8 trillion, with non-mortgage debt (credit cards, personal loans, auto loans, etc.) near $4.74 trillion.

TransUnion’s Q3 2025 Credit Industry Insights Report describes a clear “K-shaped” recovery:

- Super-prime borrowers now make up 40.9% of the market (up from 37.1% in 2019).

- Subprime originations (scores below 660) reached 14.4% — the highest share since 2019.

Equifax December 2025 data shows total debt continuing to edge higher, while severe delinquencies (60+ days past due) remain mixed but mostly flat-to-slightly-better year-over-year in several categories.

Quick Highlights

- Credit card balances: ~$1.08–1.28 trillion (up 4–5.5% YoY)

- Unsecured personal loan balances: ~$253 billion, with strong subprime growth

- Overall 60+ DPD rate: ~1.61%

- Average credit score dipped to 700 (VantageScore)

Growth has been steady, but pressures are building — especially in subprime pockets — as high interest rates and inflation continue to squeeze households.

Takeaway: Delinquencies have largely plateaued at levels well above pre-pandemic norms. Unsecured categories remain resilient, but subprime borrowers are clearly more exposed.

2. What’s Driving the Subprime Unsecured Lending Boom?

Consumers are turning to credit cards and personal loans for liquidity and debt refinancing.

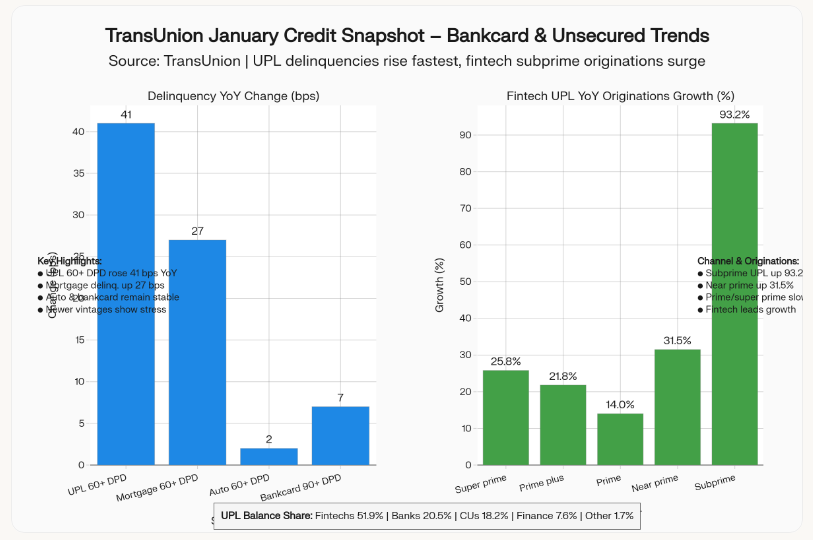

- Fintechs now control ~53% of unsecured personal loan balances through fast, data-driven approvals.

- Credit unions hold ~18% and banks ~21%, both expanding digital and embedded-finance offerings after prior pullbacks.

Traditional banks tightened underwriting, so demand flowed to faster, more flexible alternatives. Subprime originations rose 2.9% YoY in late 2024 — the first increase in eight quarters — with deep-subprime borrowers (<580) increasing activity in auto and unsecured lending.

3. The Private Credit Connection: Blue Owl as an Early Warning

The $3 trillion private credit market underpins much of fintech and non-bank lending.

In February 2026, Blue Owl Capital permanently gated redemptions on its $1.7 billion OBDC II retail fund following $150 million in investor outflows — a move reminiscent of early liquidity crunches in past credit cycles.

Why it matters: Prolonged investor withdrawals could raise funding costs or cut access for fintechs and credit unions, tightening credit flows to subprime borrowers and amplifying risk if delinquencies climb.

4. The Main Emerging Risks

No immediate crisis is visible, but interlinked risks are building:

- Delinquency spikes: Subprime rates softened to 11.4% but remain high. Unsecured defaults hit harder, lacking collateral.

Evidence: Auto delinquencies already near Great Financial Crisis peaks. - Funding squeezes: Redemption gates and BDC outflows restrict capital to lenders.

Evidence: Billions in investor withdrawals from private credit funds in late 2025. - Regulatory & cyber exposure: Rapid digital growth heightens fraud and systemic fairness concerns.

Evidence: Fraud and liquidity flagged as top threats in 2025 risk surveys. - Systemic spillover: Fintechs and private credit are tightly connected, creating transmission risk.

Evidence: Forecasts show only partial easing — auto delinquencies still near 1.54% for 2026.

5. Visual: Credit Card Delinquency Trends

A conceptual chart would show the post-pandemic surge (2022–2023) followed by a 2025 flattening, using Federal Reserve 30+ DPD and Equifax 60+ DPD data.

This visualization underscores the pressure points in unsecured lending — especially among subprime borrowers.

Conclusion: Proceed with Caution

The rapid expansion of subprime unsecured lending has improved credit access but raised systemic risk. Elevated delinquencies and private credit stress — with Blue Owl’s move as a key signal — warrant a cautious outlook.

Next Steps

- Lenders: Strengthen models, diversify funding sources, refine subprime underwriting.

- Regulators: Increase transparency in non-bank and fintech lending.

- Everyone: Act early to avoid sharper turbulence in 2026.

By tackling these vulnerabilities proactively, the industry can sustain greater access to credit while avoiding past cycle mistakes.

Sign up at RiskInMind.ai(https://www.riskinmind.ai) for a quick demo to see how you can mitigate risk in underwriting and portfolio management.